3.2.3 Receipt and Review of Statutory Reports

The financial reports submitted by electoral contestants as regards the financing of their election campaigns and by political parties about the financing of their routine activities are the primary source of information at your disposal to carry out your supervision tasks.

The existence of internal procedures that set out rules pertaining to receipt and review of financial reports will help guide staff members on how to handle statutory reports within a clear, impartial and coherent framework and for your institution to demonstrate fairness, impartiality and quality control at all times.

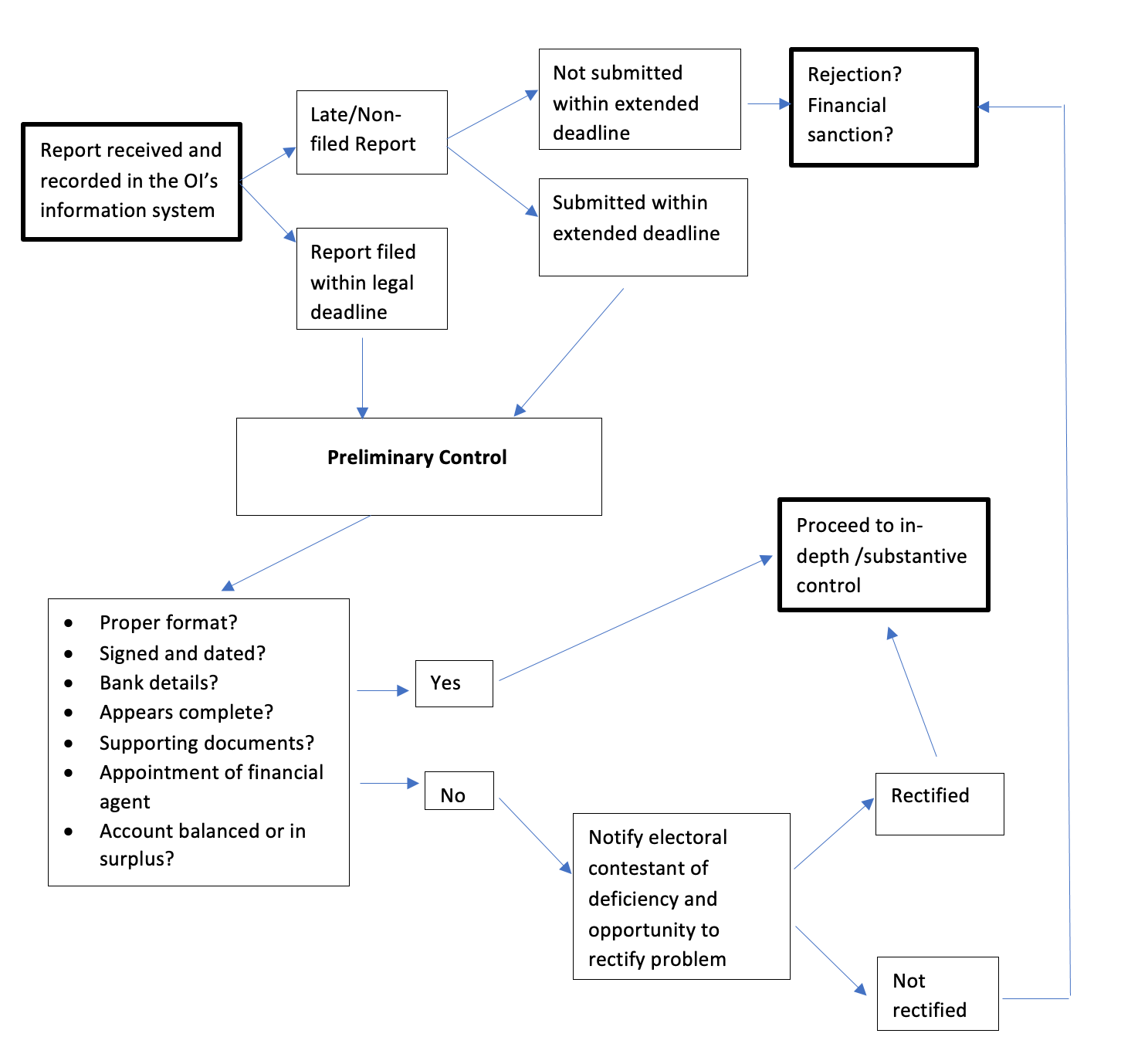

It is good practice to record all financial reports submitted to the oversight institution, whether within or after the legal deadline. Ideally, all reports received should be recorded in an IT-based system to flag any late filing and facilitate the review process.

Depending on your country’s legislation and institution’s remit, the review of the financial reports could encompass distinct phases of control or be undertaken all at once. Whatever the rules in force, it is good practice to notify to the electoral contestants and political parties all irregularities, discrepancies or breaches that could lead to the launching of an investigation and / or the referral of the case to law enforcement agencies or prosecutorial authorities.

3.2.3.1 Receipt of statutory reports

Depending on the applicable legal framework, financial reports can be submitted in hard copies, through entries on the oversight body’s website and/ or electronic formats. In order to enhance compliance with reporting requirements, a significant number of oversight institutions put out reminders on their website or in their manuals/ handbooks regarding the filing deadlines of the financial reports (see the Election Canada website and this document explaining the process on the CNCCPF website in France (CNCCFP website.pdf). This can also be accompanied by the sending of letters or emails to the electoral contestants recalling their obligations and the reporting timeframe at the beginning or just before the end of the election campaign. While it is the responsibility of the reporting entity to submit reports correctly and on time, non-compliance reflects badly on the oversight institution, and it should therefore spend much effort on ensuring a high compliance rate.

Ideally all received reports should be recorded in your register or intranet/ information system with the mention of the submission date of the hard copy (if applicable, mention of the submission date of the electronic date as well) and be assigned a file number. The use of e-reporting systems if you have such a system in place will help flag irregularities as regards the receipt of financial reports.

Statutory reports can be submitted within the legal deadline or can also be lodged after the legal deadline or not submitted at all. The late filing or absence of submission of reports might trigger the sending of a request by your institution to ask the political party/ candidate to regularize the situation or to warn to sanction the identified irregularity.

3.2.3.2 Review of statutory reports

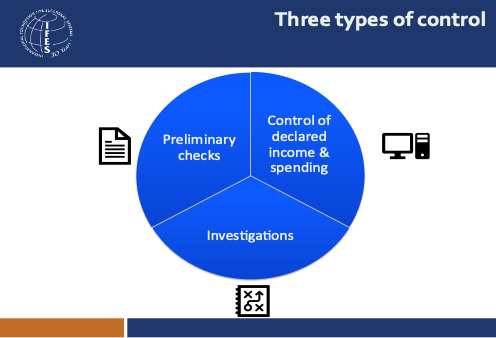

The review of financial reports is often composed of three distinct phases of which the first two always occur: Three types of control.pdf.

- The preliminary control of submitted reports to detect any readily apparent problems;

- the carrying out of in-depth controls taking into account the different sources of information the oversight body has at its disposal

- The investigation of irregularities/ violations detected during one of the first two phases

Prioritization Risk register

Some oversight institutions use a risk register to rationalize and prioritize their workload. This internal document helps identify risk areas and red flags (Table of risk areas AND red flags.pdf), whose the likelihood to occur and the potential impact on the campaign/ political party routine activity are the most likely to have a significant influence on the electoral or political process. The risk criteria elaborated by the oversight institutions aim to determine:

- who is subject to its control taking into account written, objective and clear factors, such as the financial resourcesof the electoral contestants(main political parties/ candidates with significant support and electoral results) or the apparition of new political actors (newcomers with some strong and wealthy supporters)

- the kind of activity to control as regards income, such as donation or loan patterns, the use of payment platforms bundling donations for a specific electoral contestant to collect donations;

- the kind of spending to control, such as electoral rallies/ meetings (potential cases of ASR, vote buying); outdoor billboards; digital spending and the use of portals for paid political advertising taking into account the importance, sensitivity, impact on the electorate;

- when the control happens; before, during and after the election campaign or on a rotating basis for political party routine activity.

Although it has been discontinued, please see the risk profile system used by the Electoral Commission of the UK.

Preliminary analysis: detection of readily apparent problems

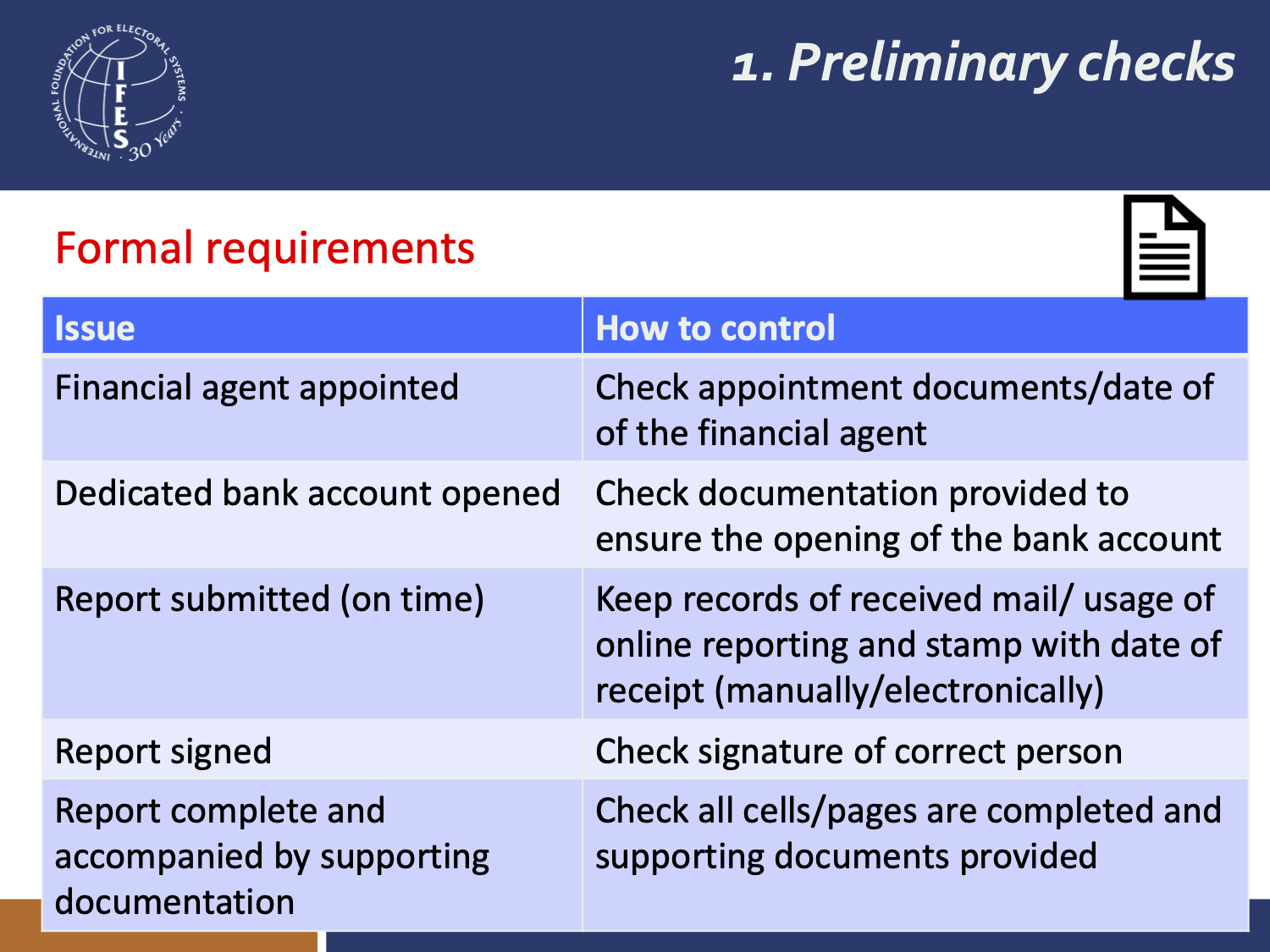

The goal of preliminary control is to ensure that the finance reports meet formal requirements and to detect readily apparent problems using no other data than the reports themselves.

Formal requirements

| Issue | How to control |

| Financial agent appointed | Check appointment documents/date of the financial agent |

| Dedicated bank account opened | Check documentation provided to ensure the opening of the bank account |

| Report submitted (on time) | Keep records of received mail/usage of online reporting and stamp witih date of receipt (manually/electronically) |

| Report signed | Check signature of correct person included |

| Report complete and accompanied by supporting documentation | Check all cells/pages are completed and supporting documents are provided |

When carrying out the preliminary verification, you may want to check whether:

- an official agent responsible for financial matters has been appointed if the law foresees such an obligation;

- the report has been submitted within the legal deadline, in the prescribed formats in the legislation and signed by the competent person/ people;

- the report appears to complete (all relevant pages/ cells are completed) and is accompanied by all supporting documentation.

The existence of checklists / dropdown menus in your information system might help your staff members carry out this part of the control process. Some options presented below might be irrelevant depending on the existing political finance regulations into force in your country.

| Yes | No | |

|---|---|---|

| Format of reports submitted | ||

| Was the report submitted on time? | ||

| Has the reporting template been used? | ||

| Has the report been submitted in hard copy and/or electronically and/or through entries on your website? | ||

| Have all pages been completed/ filled out? | ||

| Is the report signed by the competent person/ people? | ||

| Content of reports submitted | ||

| When was the financial agent appointed? If applicable | ||

| Does the bank account number provided match the account designated by the political party/ candidate? If applicable | ||

| Is the election finance campaign report balanced or in surplus? | ||

| Does the total amount of in-kind contributions correspond to the total amount of in-kind expenditure? | ||

| Are the declared expenses within the spending limit? | ||

| Supporting documentation | ||

| Are the bank statements provided? | ||

| Are donor declarations provided? If applicable | ||

| Are contracts for goods and services provided? | ||

| Are invoices for goods and services provided? | ||

| Is the documentation pertaining to the valuation and calculation of in-kind donation/ spending reported in the report provided? | ||

| Are specimens of electoral materials provided? | ||

It is good practice to prepare a list of all entities required to submit reports in order to keep records of the ones who have filed within/ after the legal deadline or any agreed extended deadline and have not filed, especially if your institution is not equipped with an online reporting system.

Depending on the regulations in place in your country, the preliminary control may be undertaken of all reports filed whether within the legal deadline or late. Regardless of the submission format used, it is important to keep records of all received mails and e-mails, together with the manual stamp / electronic submission date of receipt of the reports.

During this first phase of control, the staff members of your institution may detect irregularities or inaccuracies that will need to be regularized. Your internal procedures may foresee the possibility to ask for further information, accept or reject the account. In case it is concluded that the report should be rejected, potentially after requesting further information/ regularization, it is good practice to send to the concerned electoral contestant a letter specifying the defects found, the steps the political party/ candidate should take and a deadline for doing so, and the potential legal consequences for failing to take the specified action.

In-depth control of final election finance reports

The in-depth or substantive control of declared income and spending aims to check the compliance by political parties and candidates with provisions of the legal framework. To do so, oversight bodies usually check the submitted reports and compare the reported financial information with other data sources to control accuracy.

To this end, your institutions may carry out some or all of the tasks below:

- controlling the documentation of income and ensuring the permissibility of donors and that donations (loans) made are within the legal limit(s);

- controlling the documentation of spending, checking that expenses have been incurred for electoral purposes (for elections) and ensuring that reported expenses are within the spending limit;

- checking whether the total amounts of income and spending declared by political parties/ candidates match the amounts mentioned in the supporting documentation and the accounting books;

- comparing the amounts declared by political parties/ candidates with any information contained in the interim reports (if applicable), gathered throughout the campaign by filed monitors (if applicable) or data gathered by/ available to your institution or contained in the complaints/denunciations received;

- controlling that the finance reports, based on the information submitted and reported, do not reveal any violations of the law pertaining to the sources of income or expenditures.

You can find a detailed description of the approach to checking campaign finance reports by the oversight institution in France (Country example / France - In-depth control of final election finance reports.pdf), including their checklist for controlling political party annual financial reports (Checklist for controlling political party annual financial reports.pdf).

The Agency for the Prevention of Corruption in Montenegro has also provided a description of how they review received financial reports (Country example / Montenegro – Agency for the Prevention of Corruption’s review process of the financial reports submitted by political entities and on cooperation mechanisms with the State Audit Institution (SAI).pdf).

-

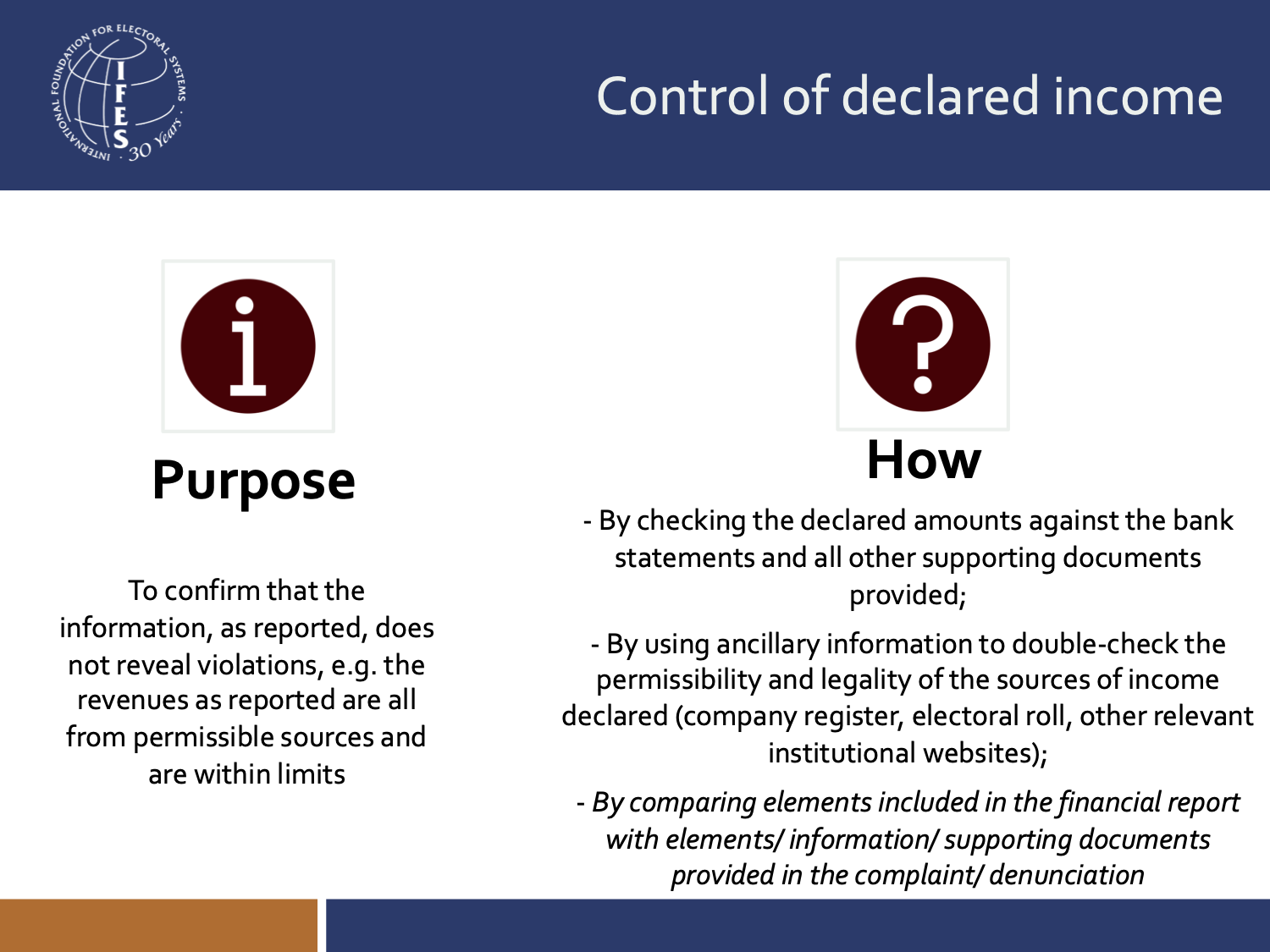

Control of declared income

The main goal of the control of declared income is to verify whether the sources of funding come from permissible contributors and whether the amounts declared match the amounts mentioned in the supporting documents and bank statements. This control is based on the information and documents submitted by the political party/ candidate in their reports, but also resorts to the use of bank statements and all other relevant documents (loan documentation, institutional registries, etc.) to check the permissibility and legality of the sources of financing declared.

The first step consists generally of checking the amounts declared by type of revenue, i.e. donations, loans, self-financing, political party contributions/ income generating activities/ membership fees and ensure that the total of declared income matches the individual amount for each type of reported source of financing. Once the first series of checks is done, the second step usually consists of reviewing the correspondence between the information contained in the report and the information contained in the supporting documents. To do so, it is good practice to check:

→ each source of income reported against the bank statements and ensure that:

- each monetary income collected and reported is traceable and corresponds to a single financial transaction on the bank statement(s);

- the date of each transaction clearly mentioned and checkable;

- the amounts declared match;

- the origin of the income declared (name of the donor/ lender/ party contribution/ party member/ source of the party income) aligns with the information mentioned on the bank statement(s) and/or on the institutional registers/ registries to potentially detect whether impermissible donors (foreign/ anonymous donors, donations made in the name of another).

→ each in-kind contribution reported against the supporting documents. Each in-kind contribution should have its equivalence in spending in order to detect whether there are unreported/ underestimated/ undeclared in-kind contributions or in-kind contribution disguised as volunteer activity.

Having checklists/ dropdown menus in your information system constitutes a very helpful controlling tool to enable the control over the permissibility requirements and the compliance with donation/ loans limits. There are a variety of methods used for checking the permissibility of donations depending on country context and other factors - the approach used in several countries is outlined further in this document (Case study on permissibility of donations.pdf). Depending on the regulatory situation in your country, controls of income may also include the use of certain forms of bank transactions, the use of cryptocurrencies and related issues.

Some options presented below might be irrelevant depending on the existing political finance regulations in force in your country.

| Requirement | How to control? What to control? |

|---|---|

|

|

|

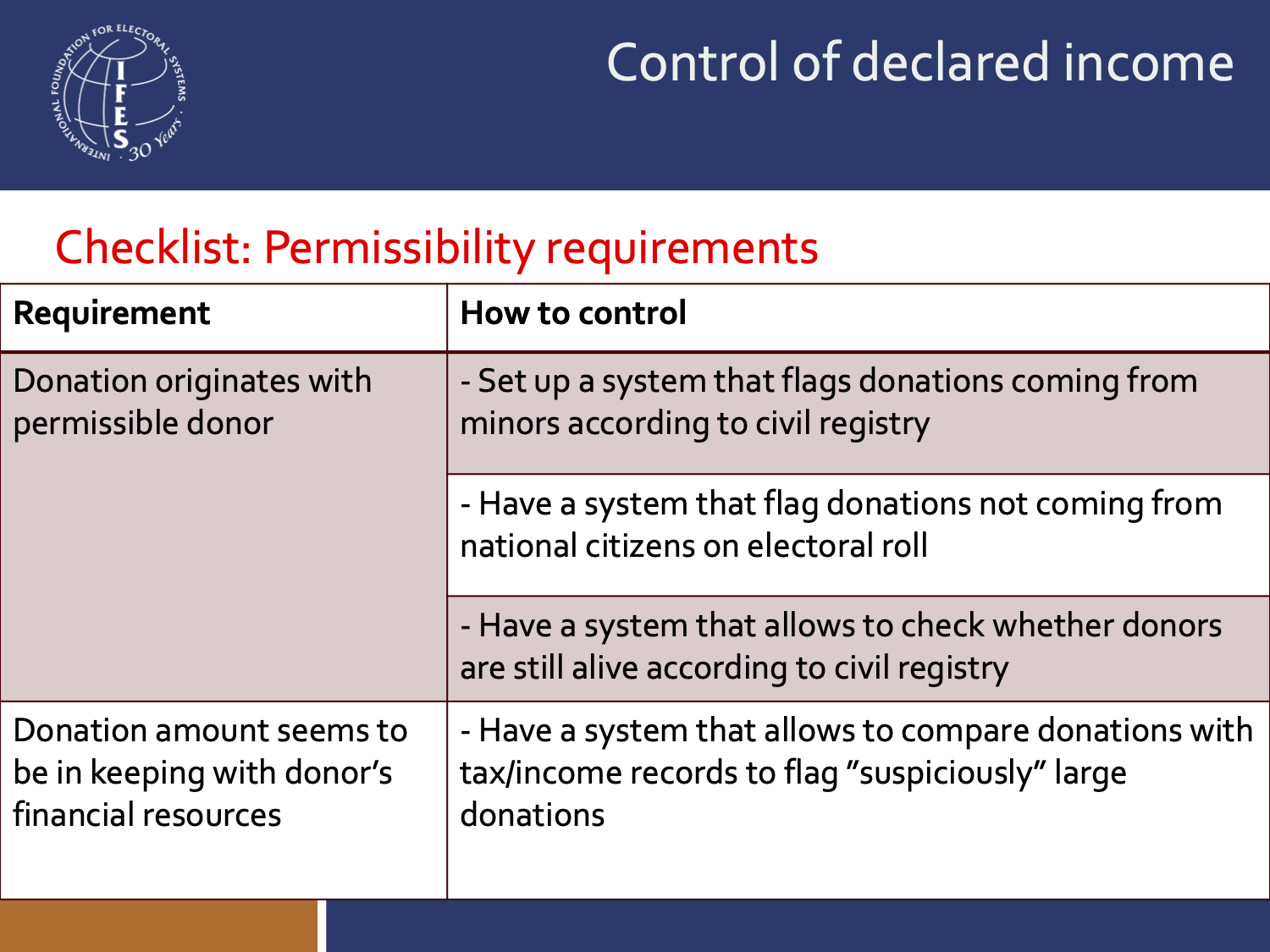

| Donation originates with permissible donor (individuals) (nationality, age, situation) |

Cross-check with social registry Cross-check with civil service registry Cross-check with electoral roll to detect donations from foreigners, minors. |

| Donation amount seems to be in keeping with donor's financial resources | Cross-check with tax registry and tax/income records to detect "suspiciously" large donations |

| Donation originates with permissible donor (domestic legal entity, no government contracts) |

Cross-check with registry of legal entities and/or company registry |

| Donations within legal limits | Aggregate donations from a same donor - Calculate total value of all donations from one donor to the same recipient |

|

|

|

| Loan originates with permissible donor | Check the identification number on the appropriate state register |

| Loan amount seems to be in keeping with lender's financial resources | Compare loans with tax/income records to flag "suspiciously" large loans (that could possibly be written off) |

| Terms of loan consistent with fiscal legislation? | |

| Loans within legal limits | If applicable |

|

|

|

| Self-funding seems to be in keeping with candidate's financial resources | Compare personal funding amount with tax/income records to assess if there are red flags about it being personal funding. |

|

|

|

| Funds transferred should be from commercial activities such as publications, printing presses, services, leasing, membership fees | For membership fees, trace source of funding back to party members. Cross-check with last annual financial statement |

| Political party donation | Review land cross-check with last annual financial statement |

-

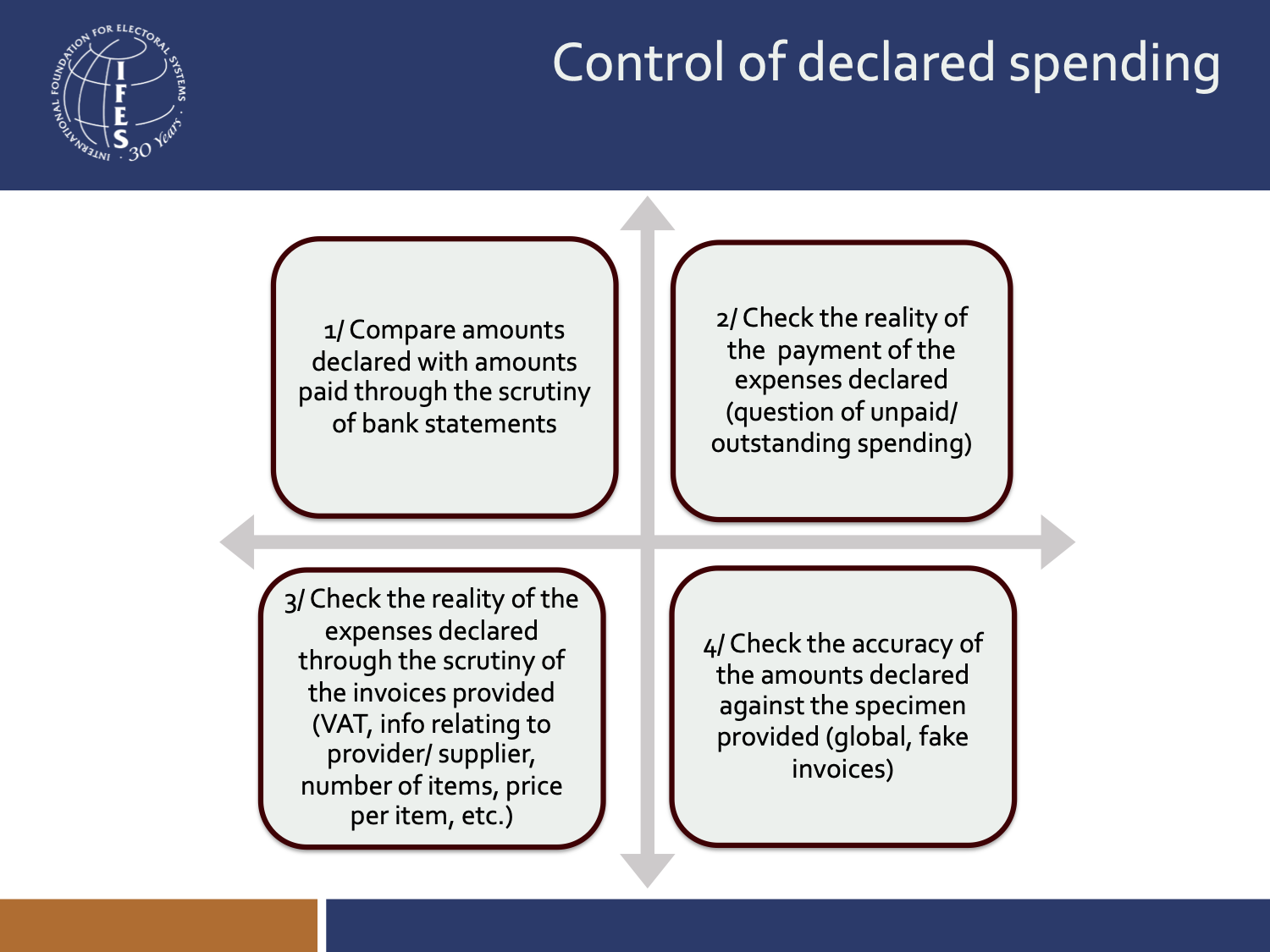

Control of declared spending

The main goal of the control of declared spending is to check whether reported expenses were incurred for electoral purposes / for political party routine activity purposes and to detect any potential overspending, underestimated spending, unreported spending or illegal expenses (ASR / vote buying) of submitted financial reports. This control is based on the information and documents submitted by political parties/ candidates in their reports, but also on bank statements and all other relevant documents (invoices, contracts, (electoral) specimen and materials, etc.) to check the legality and accuracy of the spending reported. For a practical case study exploring the review of overspending by the then French President Sarkozy, see here: Case study on overspending.pdf.

The first step aims to check that all categories of spending are duly reported and that amounts of the different categories of expenses, whether paid or in-kind expenditure, add up.

Once this step completed, the second phase of this control generally consists of assessing the validity and accuracy of the spending declared by:

- comparing each declared expenditure amount with the amount shown paid in the bank statement;

- checking the accuracy of the amount declared against the specimen provided (invoices, quotes);

- confirming that expenses declared have actually been paid (e.g. no outstanding or unpaid debts) by cross-referencing with bank statements;

- controlling the invoices to ensure the validity of the declared expenditure (e.g. VAT, information related to vendors/suppliers; checking that the quantity of items ordered or the scope of services provided reflect reality and that the price per item/service appears reasonable);

- establishing that the spending declared has been incurred for electoral purposes (for elections);

- check that the declared expenses are within the spending limit (for elections) and that the spending on certain category (such as media advertising) must not exceed certain value (e.g. Poland, Lithuania)

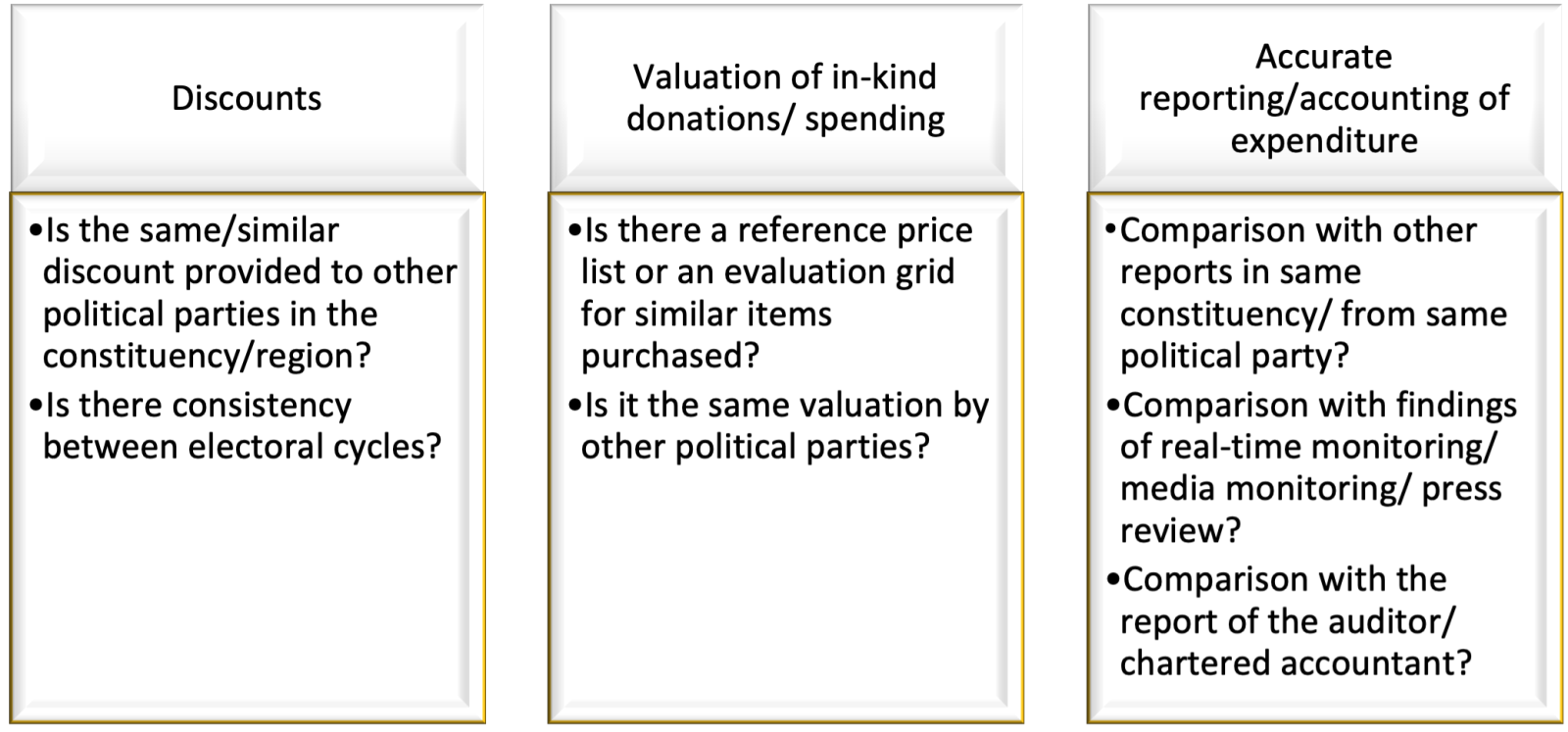

The analysis of declared spending can then lead to draw conclusions and compare reported amounts between different election campaign finance reports and help your staff members flag elements that might appear suspicious, such as:

-

Case processing

At the end of the control process, you are most likely to find out the following types of irregularities:

- Absence of supporting documentation;

- Discrepancies/ inconsistencies between amounts declared and supporting documents provided.

- Donations above the limit or not made in the dedicated bank account;

- Problem with the valuation of in-kind contributions/ expenses;

- Problem of accounting of expenses declared (under/over estimation);

- Impermissible donations;

- Problem of tax invoices/ global invoices;

- Absence of electoral nature of expenses declared (for elections);

- Omission/ partial accounting of electoral expenses (for elections).

It is good practice that at the end of the in-depth control, staff members draft a report highlighting the issues identified during the control and documents the results of the review process. It is common that the review process be accompanied by the carrying out of administrative/ adversarial proceedings to seek explanation from political parties/ candidates and identify information and documents that are needed to complete the substantive control. Regardless of your internal procedures, it is critical that the letter sets a deadline for the political party/ candidate’s reply and advises what subsequent action may be taken in case of failure to address the issue(s)/ answer the request

As part of the in-depth control, your staff members will need to consider the findings and conclusions set out in the financial monitor and auditor reports (if applicable) to assess:

- whether the election finance report substantiates or negates the findings raised in the monitor/auditor report;

- whether the monitor/auditor reports raises novel legal issues that need to be referred before proceeding further.

Depending on your remit, you may also take into account information contained in complaints and obtained from any person/entity who may reasonably have relevant information (broadest power) or from political parties/donors (more limited).